The retail sector in Saudi Arabia: is recovery in sight?

By Cyrille C. Fabre, Director and head of the retail practice, Bain & Company Middle East

Expectations about the future outlook have been incredibly erratic this year. After a good start of the year, retailers became very pessimistic in Q2 with the combined effect of lockdown and VAT. In a survey that Bain & Co jointly carried out with Mukatafa in May 2020, over 50% of the retailers were expecting a 20%+ decline in sales, and 90% were considering significant restructuring. Yet, the sector performed better than expected in the second half of the year, and many retailers are now quite optimistic and re-starting store expansion. Is this optimism well placed? Can we see the light at the end of the COVID tunnel, or is it a mirage of hope?

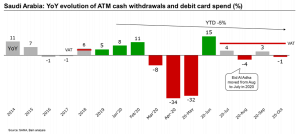

2020 has been a surprising year for the retail sector in Saudi Arabia. Statistics from SAMA on ATM cash withdrawal and debit card spending give us an idea of the evolution of consumer expenditure in the Kingdom this year. Though not perfect as it excludes credit cards, this indicator is interesting as it tracks around ~SAR50Bn of cash withdrawal and SAR28Bn of debit card spend every month.

After a strong start of the year in Jan/Feb, the market collapsed by ~30% during the lockdown and then recovered sharply in June as consumers anticipated VAT increase. Since July, the negative impact of the VAT increases have been offset by the positive effects of the lack of traveling: the market stabilized at around 1% growth vs. last year. Year to date, retail is declining by ~5%, but it could have been much worse.

Figure 1: Evolution of consumer expenditure in KSA as measured by ATM withdrawal and debit card spending

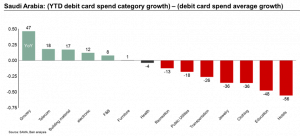

This average evolution hides significant variations across sectors. Looking at debit card spend alone (~35% of consumer spend) gives a rough idea of winning and losing sub-sectors. Because debit cards represent a fast-growing consumer expenditure share, we need to interpret this data carefully and look only at the relative difference between sectors and not at absolute growth. Figure 2 below shows the relative growth of debit card expenditures in each sector. Unsurprisingly, grocery (notably staple food), electronics, telecom, and home improvement have been the primary beneficiaries of the pandemics. Conversely, sectors like hotels, clothing, jewelry, and transportation have suffered so much in the first part of the year that the recent recovery is not enough to save the year.

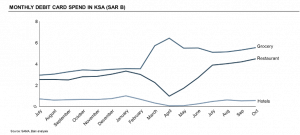

As shown in figure 3, the restaurant sector has experienced such a spectacular rebound since July that the year will not be disastrous after all. This astonishing performance reflects both demand and supply dynamics. On the demand side, Saudi residents could hardly travel, triggered additional demand for entertainment and restaurants in the Kingdom. On the supply side, the development of new destination dining venues has also stimulated the market.

Figure 2: Relative evolution of retail sub-sectors

Figure 3: Evolution of consumer expenditure on food by sub-sector

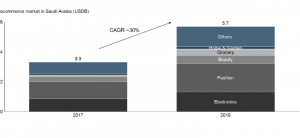

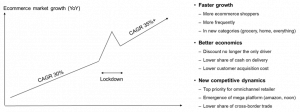

The retail sector that grew the most this year is by far e-commerce. Pre-covid, e-commerce was already a booming market. From 2017 to 2019, the e-commerce market in Saudi Arabia grew at 30% p.a. to reach $5.75Bn (including all retail goods but excluding food service, digital media, and travel). In two years, penetration has increased from 4% to ~6.5%, which remains well below developed economy benchmarks (17% in the USA, 20% in the UK, 12% in the EU).

Figure 4: Evolution of the e-commerce market in Saudi Arabia 2017-19

Covid brutally re-shaped the market. Market growth accelerated further as new consumers tried e-commerce for the first time, and as frequency increased. Shoppers started buying online for everything, and categories that were under-developed like Grocery and Home started booming at 300%+. Some of the e-commerce booms subsided after the end of the lockdown, but the market stabilized at a much higher level than before. Data is not yet available for an exact quantification, but figure 5 below gives an illustrative estimate of the overall trend.

Figure 5: Impact of Covid on the e-commerce market in Saudi Arabia

Now that we reviewed the evolution in 2020, how do we think the market will evolve in 2021? Is the current wave of optimism fully justified? Beyond quantitative growth, what changes can we detect in the market?

On the positive side, there has indeed been positive momentum in the last four months, and consumer confidence seems improving from the low point of July 2020. Some of the 2020 H2 growth drivers may continue in 2021: savings in Q2 2020 may not be entirely spent. The repatriation of the spending done by Saudi abroad may continue in 2021 as traveling will remain difficult for a while. An increase in female employment and the minimum salary can bring additional purchasing power to the households. On the supply side, new exciting retail venues will open in the coming years, and many new brands – often homegrown – are entering the market. There is also considerable scope for modern retailers in specific industries, like grocery, to gain share over traditional retail.

Yet, there are also reasons to be careful. Consumer purchasing power has been reduced by ~12%+ as a result of the VAT increase and allowance reduction. Unemployment remains relatively high, and there is limited potential to increase consumer debt. Beyond the effect on market volume, retailers are likely to face a headwind on their profitability. Despite e-commerce, new stores continue to open every year, and sales per store are dropping alarmingly across many sectors. This trend is compounded by the fact that traditional retail is proving more resilient than previously envisioned. Operating costs also keep increasing partly as a result of growing Saudization requirements.

The net effect of these conflicting trends are not yet clear. Optimism seems warranted for staples and entertainment, but other sectors like durable goods and automotive may continue to suffer.

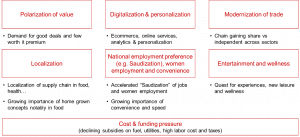

Beyond these quantitative challenges, we should also expect some qualitative changes from the 2020 crisis. Figure 6 summarizes the key trends that we see for 2021. Most of these changes are about a steep acceleration of previous trends.

Figure 6: Qualitative retail trends in Saudi Arabia in 2021

Given these quantitative and qualitative trends, a few priorities are emerging for retailers:

- Focus on leading brands as they tend to over-perform in uncertain times

- Innovate around new consumer needs: consumers’ lifestyles are evolving and becoming more diverse. There is enormous scope for new propositions not yet available in Saudi Arabia.

- Embrace omnichannel as e-commerce is the fastest-growing channel

- Be lean and optimize cost to offset the impact of cost inflation and declining sales/store

- Develop the new generation of Saudi talents

- Expand store selectively to avoid saturation and consider M&A to consolidate market position

I have seen in 2020 many Saudi retailers embracing these priorities with a renewed sense of importance and focus. This new strategic plan, combined with the right support from the Saudi Government, can make us indeed more optimistic about the future.

Mukatafa has partnered with Bain & Co. quarterly to align on the recent sector trends. This article is the first of many from Monsieur Cyrille Fabre, so continue to follow for more of this expert’s reflections.

Cyrille Fabre is a partner in Bain & Company’s Middle East offices. He leads Bain’s Consumer Products and Retail practices and family businesses in the Middle East.

Cyrille has 20 years of management consulting experience and delivers strategies that work for leading businesses.

He primarily advises retailers and consumer products companies on strategy, customer experience, and performance improvement. He has also developed specific expertise across the Middle East food sector, from producer to retailer.

Additionally, Cyrille works with economic development agencies to address topics such as retail sector strategies, food security, and industrialization in the GCC region.

He has applied his management consulting expertise globally with Bain, having also worked in the firm’s Brussels office.

Cyrille’s insights have been published and quoted in publications including Forbes, Gulf News, The National, Al Bayan, and Saudi Gazette.